|

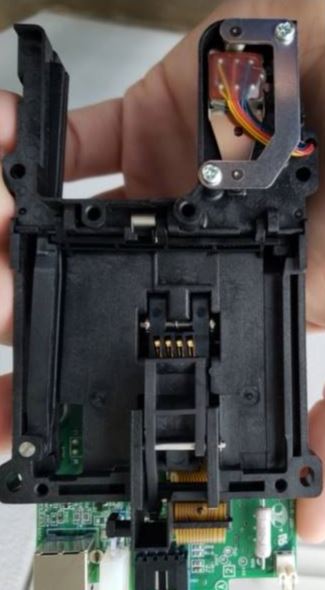

Very often the most clever component of your typical ATM skimming attack is the hidden pinhole camera used to record customers entering their PINs. These little video bandits can be hidden 100 different ways, but they’re frequently disguised as ATM security features — such as an extra PIN pad privacy cover, or an all-in-one skimmer over the green flashing card acceptance slot at the ATM. And sometimes, the scammers just hijack the security camera built into the ATM itself. Below is the hidden back-end of a skimmer found last month placed over top of the customer-facing security camera at a drive-up bank ATM in Hurst, Texas. The camera components (shown below in green and red) were angled toward the cash’s machine’s PIN pad to record victims entering their PINs. Wish I had a picture of this thing attached to the ATM.

This hidden camera was fixed to the underside of a fake lens cover for the skimmed ATM’s built-in security camera. Image: Hurst Police. The clever PIN grabber was paired with an “insert skimmer,” a wafer-thin, usually metallic and battery powered skimmer made to be fitted straight into the mouth of the ATM’s card acceptance slot, so that the card skimmer cannot be seen from outside of the compromised ATM.

The insert skimmer, seen as inserted into the card acceptance device in the hacked ATM. Image: Hurst PD.

For reference, here’s a similar card acceptance slot, minus the skimmer.

An unaltered ATM card acceptance slot (without insert skimmer). Police in Hurst, Texas released a photo taken from footage showing what appears to be a young woman affixing the camera skimmer to the drive-up ATM. They said she was driving a blue Ford Expedition with silver trim on the lower portion of the vehicle.

The skimmer crooks seem to realize that far fewer people are going to cover their hand when entering a PIN at drive-up ATMs. Often the machine is either too high or too low for the driver-side window, and covering the PIN pad to guard against hidden cameras can be a difficult reach for a lot of people. Nevertheless, covering the PIN pad with a hand, wallet or purse while you enter the PIN is one of the easiest ways to block skimming attacks. The skimmer scammers don’t just want your bank card: They want your PIN so they can create an exact copy of the card and use it at another ATM to empty your checking or savings account. So don’t be like the parade of people in these videos from hidden cameras at hacked ATMs who never once covered the PIN pad. Further reading: Woman Caught on Video Installing Skimmer Outside Bank’s ATM in Hurst from https://krebsonsecurity.com/2019/03/insert-skimmer-camera-cover-pin-stealer/

0 Comments

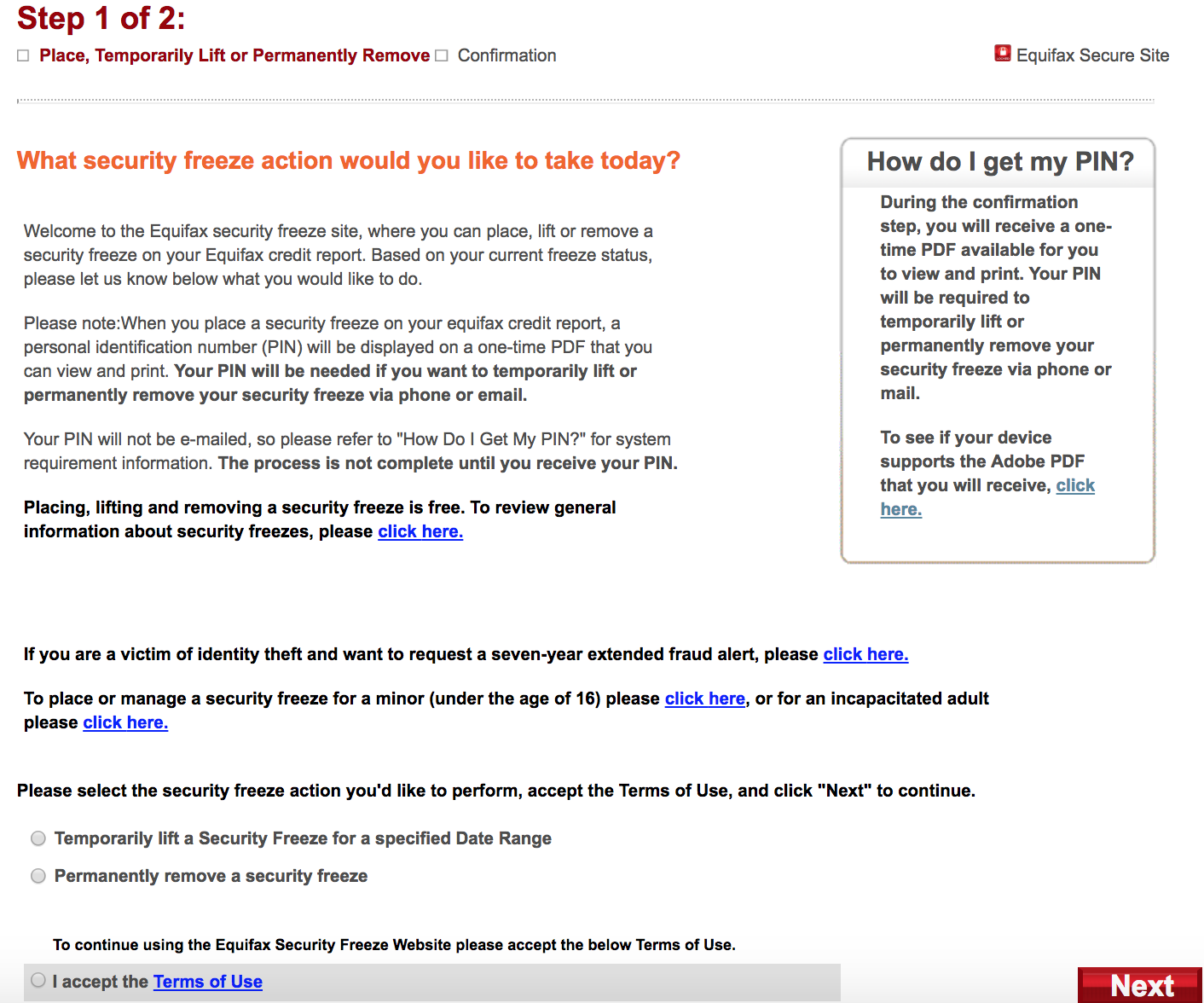

Most people who have frozen their credit files with Equifax have been issued a numeric Personal Identification Number (PIN) which is supposed to be required before a freeze can be lifted or thawed. Unfortunately, if you don’t already have an account at the credit bureau’s new myEquifax portal, it may be simple for identity thieves to lift an existing credit freeze at Equifax and bypass the PIN armed with little more than your, name, Social Security number and birthday. Consumers in every U.S. state can now freeze their credit files for free with Equifax and two other major bureaus (Trans Union and Experian). A freeze makes it much harder for identity thieves to open new lines of credit in your name.

In the wake of Equifax’s epic 2017 data breach impacting some 148 million Americans, many people did freeze their credit files at the big three in response. But Equifax has changed a few things since then. Seeking to manage my own credit freeze at equifax.com as I’d done in years past, I was steered toward creating an account at myequifax.com, which I was shocked to find I did previously possess. Getting an account at myequifax.com was easy. In fact, it was too easy. The portal asked me for an email address and suggested a longish, randomized password, which I accepted. I chose an old email address that I knew wasn’t directly tied to my real-life identity. The next page asked me enter my SSN and date of birth, and to share a phone number (sharing was optional, so I didn’t). SSN and DOB data is widely available for sale in the cybercrime underground on almost all U.S. citizens. This has been the reality for years, and was so well before Equifax announced its big 2017 breach. myEquifax said it couldn’t verify that my email address belonged to the Brian Krebs at that SSN and DOB. It then asked a series of four security questions — so-called “knowledge-based authentication” or KBA questions designed to see if I can about my recent financial history. In general, the data being asked about in these KBA quizzes is culled from public records, meaning that this information likely is publicly available in some form — either digitally or in-person. Indeed, I have long assailed the KBA industry as creating a false sense of security that is easily bypassed by fraudsters. One potential problem with relying on KBA questions to authenticate consumers online is that so much of the information needed to successfully guess the answers to those multiple-choice questions is now indexed or exposed by search engines, social networks and third-party services online — both criminal and commercial. The first three multiple-guess questions myEquifax asked were about loans or debts that I have never owed. Thus, the answer to the first three KBA questions asked was, “none of the above.” The final question asked for the name of our last mortgage company. Again, information that is not hard to find. Satisfied with my answers, Equifax informed me that yes indeed I was Brian Krebs and that I could now manage my existing freeze with the company. After requesting a thaw, I was brought to a vintage Equifax page that looked nothing like myEquifax’s sunnier new online plumage.

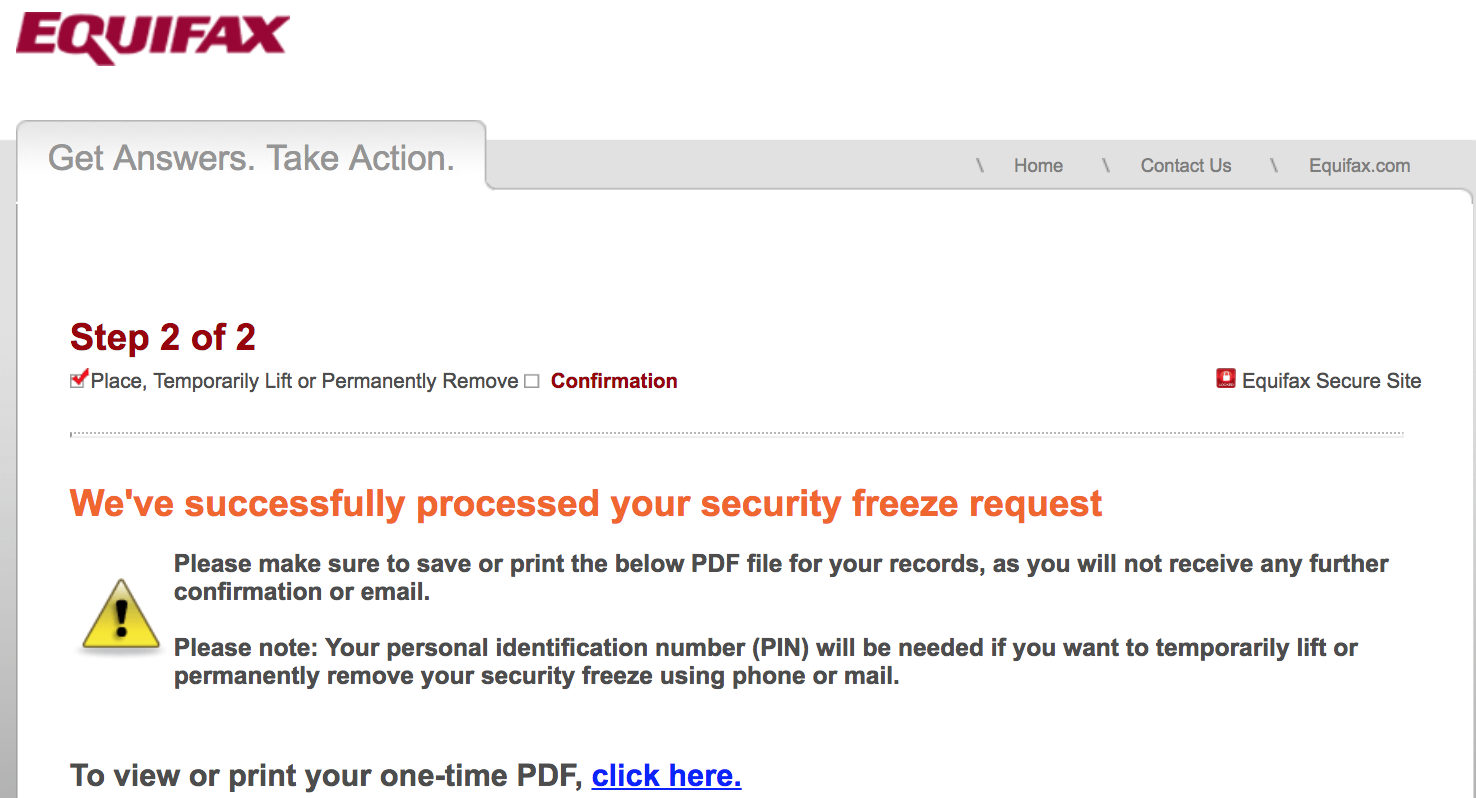

Equifax’s site says it will require users requesting changes to an existing credit freeze to have access to their freeze PIN and be ready to supply it. But Equifax never actually asks for the PIN. This page informed me that if I previously secured a freeze of my credit file with Equifax and been given a PIN needed to undo that status in any way, that I should be ready to provide said information if I was requesting changes via phone or email. In other words, credit freezes and thaws requested via myExquifax don’t require users to supply any pre-existing PIN. Fine, I said. Let’s do this. myEquifax then asked for the date range requested to thaw my credit freeze. Submit. “We’ve successfully processed your security freeze request!,” the site declared. This also was exclaimed in an email to the random old address I’d used at myEquifax, although the site never once made any attempt to validate that I had access to this inbox, something that could be done by simply sending a confirmation link that needs to be clicked to activate the account. In addition, I noticed Equifax added my old mobile number to my account, even though I never supplied this information and was not using this phone when I created the myEquifax account.

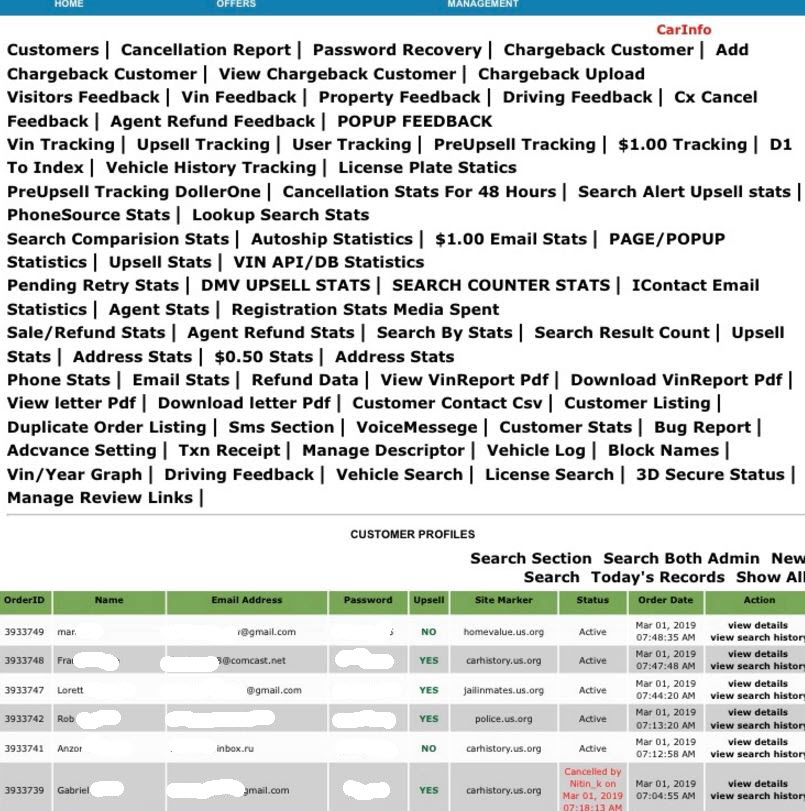

Successfully unfreezing (temporarily thawing) my credit freeze did not require me to ever supply my previously-issued freeze PIN from Equifax. Anyone who knew the vaguest and most knowable details about me could have done the same. myEquifax.com does not currently seek to verify the account by requesting confirmation via a phone call or text to the phone number associated with the account (also, recall that even providing a phone number was optional). Happily, I did discover then when I used a different computer and Internet address to try to open up another account under my name, date of birth and SSN, it informed me that a profile already existed for this information. This suggests that signing up at myEquifax is probably a good idea, given that the alternative is more risky. It was way too easy to create my account, but I’m not saying everyone will be able to create one online. In testing with several readers over the past 24 hours, myEquifax seems to be returning a lot more error pages at the KBA stage of the process now, prompting people to try again later or make a request via email or phone. Equifax spokesperson Nancy Bistritz-Balkan said not requiring a PIN for people with existing freezes was by design. “With myEquifax, we created an online experience that enables consumers to securely and conveniently manage security freezes and fraud alerts,” Bistritz-Balkan said.. “We deployed an experience that embraces both security standards (using a multi-factor and layered approach to verify the consumer’s identity) and reflects specific consumer feedback on managing security freezes and fraud alerts online without the use of a PIN,” she continued. “The account set-up process, which involves the creation of a username and password, relies on both user inputs and other factors to securely establish, verify, and authenticate that the consumer’s identity is connected to the consumer every time.” I asked Bistritz-Balkan what else besides a username and a password the company may have meant by “multi-factor;” I’m still waiting for clarification. But I did not experience anything like multi-factor in setting up or logging into my myEquifax account. This may by closer to Equifax’s idea of multi-factor: The company told me that if I still really wanted to use my freeze PIN, I could always call their 800 number (800-349-9960) or make the request via mail. Nevermind that if I’m a bad guy looking to hack others, I’m definitely going to be using the myEquifax Web site — not the options that make me have to supply a PIN. Virtually the entire United States population in 2017 became eligible for free credit monitoring from Equifax following its 2017 breach. Credit monitoring can be useful for recovering from identity theft, but consumers should not expect these services to block new account fraud; the most they will likely do in this case is alert you after ID thieves have already opened new accounts in your name. A credit freeze does not impact your ability to use any existing financial accounts you may have, including bank and credit/debit accounts. Nor will it protect you from fraud on those existing accounts. It is mainly a way to minimize the risk that someone may be able to create new accounts in your name. If you haven’t done so lately, it might a good time to order a free copy of your credit report from annualcreditreport.com. This service entitles each consumer one free copy of their credit report annual from each of the three credit bureaus — either all at once or spread out over the year. Additional reading: Credit Freezes are Free: Let the Ice Age Begin Plant Your Flag, Mark Your Territory Experian Site Can Give Anyone Your Freeze PIN Survey: Americans Spent $1.4B on Credit Freeze Fees in Wake of Equifax Breach Equifax Breach Fallout: Your Salary History Data Broker Giants Hacked by ID Theft Service Experian Sold Access to ID Theft Service from https://krebsonsecurity.com/2019/03/myequifax-com-bypasses-credit-freeze-pin/ Cybercriminals are auctioning off access to customer information stolen from an online data broker behind a dizzying array of bait-and-switch Web sites that sell access to a vast range of data on U.S. consumers, including DMV and arrest records, genealogy reports, phone number lookups and people searches. In an ironic twist, the marketing empire that owns the hacked online properties appears to be run by a Canadian man who’s been sued for fraud by the U.S. Federal Trade Commission, Microsoft and Oprah Winfrey, to name a few. Earlier this week, a cybercriminal on a Dark Web forum posted an auction notice for access to a Web-based administrative panel for an unidentified “US Search center” that he claimed holds some four million customer records, including names, email addresses, passwords and phone numbers. The starting bid price for that auction was $800. Several screen shots shared by the seller suggested the customers in question had all purchased subscriptions to a variety of sites that aggregate and sell public records, such as dmv.us.org, carhistory.us.org, police.us.org, and criminalrecords.us.org.

A (redacted) screen shot shared by the apparent hacker who was selling access to usernames and passwords for customers of multiple data-search Web sites. A few hours of online sleuthing showed that these sites and dozens of others with similar names all at one time shared several toll-free phone numbers for customer support. The results returned by searching on those numbers suggests a singular reason this network of data-search Web sites changed their support numbers so frequently: They quickly became associated with online reports of fraud by angry customers. That’s because countless people who were enticed to pay for reports generated by these services later complained that although the sites advertised access for just $1, they were soon hit with a series of much larger charges on their credit cards. Using historic Web site registration records obtained from Domaintools.com (a former advertiser on this site), KrebsOnSecurity discovered that all of the sites linked back to two related companies — Las Vegas, Nev.-based Penguin Marketing, and Terra Marketing Group out of Alberta, Canada. Both of these entities are owned by Jesse Willms, a man The Atlantic magazine described in an unflattering January 2014 profile as “The Dark Lord of the Internet” [not to be confused with The Dark Overlord].

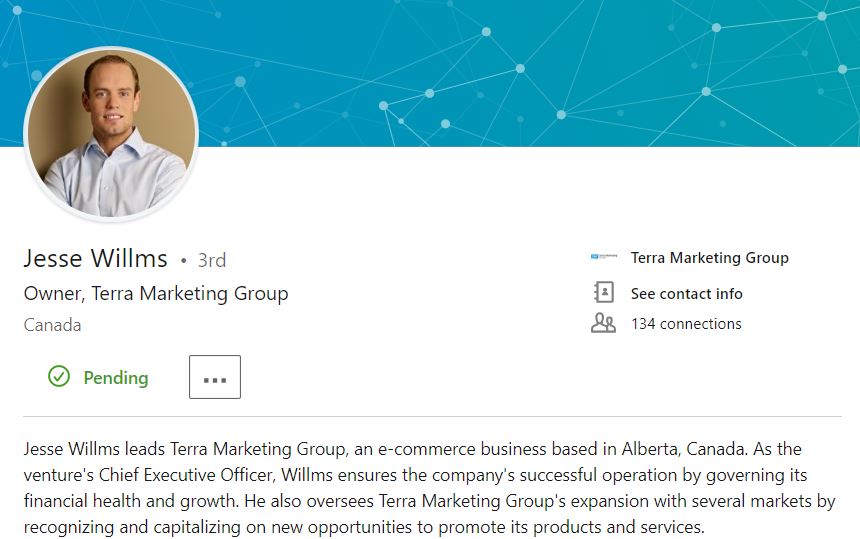

Jesse Willms’ Linkedin profile. The Atlantic pointed to a sprawling lawsuit filed by the Federal Trade Commission, which alleged that between 2007 and 2011, Willms defrauded consumers of some $467 million by enticing them to sign up for “risk free” product trials and then billing their cards recurring fees for a litany of automatically enrolled services they hadn’t noticed in the fine print. “In just a few months, Willms’ companies could charge a consumer hundreds of dollars like this, and making the flurry of debits stop was such a convoluted process for those ensnared by one of his schemes that some customers just canceled their credit cards and opened new ones,” wrote The Atlantic’s Taylor Clark. Willms’ various previous ventures reportedly extended far beyond selling access to public records. In fact, it’s likely everyone reading this story has at one time encountered an ad for one of his dodgy, bait-and-switch business schemes, The Atlantic noted:

In a separate lawsuit, Microsoft accused Willms’ businesses of trafficking in massive quantities of counterfeit copies of its software. Oprah Winfrey also sued a Willms-affiliated site (oprahsdietscecrets.com) for linking her to products and services she claimed she had never endorsed. KrebsOnSecurity reached out to multiple customers whose name, email address and cleartext passwords were exposed in the screenshot shared by the Dark Web auctioneer who apparently hacked Willms’ Web sites. All three of those who responded shared roughly the same experience: They said they’d ordered reports for specific criminal background checks from the sites on the promise of a $1 risk-free fee, never found what they were looking for, and were subsequently hit by the same merchant for credit card charges ranging from $20 to $38. I also pinged several customer support email addresses tied to the data-broker Web sites that were hacked. I received a response from a “Mike Stef,” who described himself as a Web developer for Terra Marketing Group. Stef said the screenshots appeared to be legitimate, and that the company would investigate the matter and alert affected customers if warranted. Stef told me he doubts the company has four million customers, and that the true number was probably closer to a half million. He also insisted that the panel in question did not have access to customer credit card data. Nevertheless, it appears from the evidence above that Willms and several others who were named in the FTC’s 2012 stipulated final judgment (PDF) are still up to their old tricks. The FTC has not yet responded to requests for comment. Nor has Mr. Willms. I can’t help express feeling a certain amount of schadenfreude (schadenfraud?) at the victim in this hacking case. But that amusement is tempered by the reality that the hundreds of thousands or possibly millions of people who got suckered into paying money to this company are quite likely to find themselves on the receiving end of additional phishing and fraud attacks (particularly credential stuffing) as a result of their data being auctioned off to the highest bidder. Terra Marketing Group’s Web developer Mike Stef responded to my inquiries from an email address at the domain “tmgbox.com.” That message was instrumental in identifying the connection to Willms and Terra Marketing/Penguin. In the interests of better informing people who might wish to become future customers of this group, I am publishing the list of the domains associated with tmgbox.com and its parent entities. This list may be updated periodically as new information surfaces. In case it is useful for others, KrebsOnSecurity is also publishing the results of several reverse WHOIS lookups for historic domains tied to email addresses of several people Mike Stef described as “senior customer support managers” of Terra Marketing, as these also include some interesting and related (albeit mostly dead) domains. Reverse WHOIS on Peter Graver and Jesse Willms ([email protected]) Reverse WHOIS on [email protected] Reverse WHOIS on Jason Oster ([email protected]) Public records search domains associated with Terra Marketing Group and Penguin Marketing: memberreportaccess.com from https://krebsonsecurity.com/2019/03/hackers-sell-access-to-bait-and-switch-empire/ |

ABOUT MEHi my name is Anthony I am 32 years old from Houston. I am working in local store selling electronic devices. I have been interested in eclectronics since childhood and I like to reacd about it. Archives

April 2019

Categories |

RSS Feed

RSS Feed