|

0 Comments

Richard Smith — who resigned as chief executive of big-three credit bureau Equifax this week in the wake of a data breach that exposed 143 million Social Security numbers — is slated to testify in front of no fewer than four committees on Capitol Hill next week. If I were a lawmaker, here are some of the questions I’d ask when Mr. Smith goes to Washington.

Before we delve into the questions, a bit of background is probably in order. The new interim CEO of Equifax — Paulino do Rego Barros Jr. — took to The Wall Street Journal and other media outlets this week to publish a mea culpa on all the ways Equifax failed in responding to this breach (the title of the op-ed in The Journal was literally “I’m sorry”). “We were hacked,” Barros wrote. “That’s the simple fact. But we compounded the problem with insufficient support for consumers. Our website did not function as it should have, and our call center couldn’t manage the volume of calls we received. Answers to key consumer questions were too often delayed, incomplete or both.” Barros stated that Equifax was working to roll out a new system by Jan. 31, 2018 that would let consumers “easily lock and unlock access to their Equifax credit files.” “You will be able to do this at will,” he continued. “It will be reliable, safe, and simple. Most significantly, the service will be offered free, for life.” I have argued for years that all of the data points needed for identity thieves to open new lines of credit in your name and otherwise ruin your credit score are available for sale in the cybercrime underground. To be certain, the Equifax breach holds the prospect that ID thieves could update all that stolen data with newer records. I’ve argued that the only sane response to this sorry state of affairs is for consumers to freeze their files at the bureaus, which blocks potential creditors — and ID thieves — from trashing your credit file and credit score. Equifax is not the only bureau promoting one of these lock services. Since Equifax announced its breach on Sept. 7, big-three credit bureaus Trans Union and Experian have worked feverishly to steer consumers seeking freezes toward these locks instead, arguing that they are easier to use and allow consumers to lock and unlock their credit files with little more than the press of a button on a mobile phone app. Oh, and the locks are free, whereas the bureaus can (and do) charge consumers for placing and/or thawing a freeze (the laws freeze fee laws differ from state to state). CREDIT FREEZE VS. CREDIT LOCKMy first group of questions would center around security freezes or credit freezes, and the difference between those and these credit lock services being pushed hard by the bureaus. Currently, even consumer watchdog groups say they are uncertain about the difference between a freeze and a lock. See this press release from Thursday by U.S. PIRG, the federation of state Public Interest Research Groups, for one such example. Also, I’m curious to know what percentage of Americans had a freeze prior to the breach, and how many froze their credit files (or attempted to do so) after Equifax announced the breach. The answers to these questions may help explain why the bureaus are now massively pushing their new credit lock offerings (i.e., perhaps they’re worried about the revenue hit they’ll take should a significant percentage of Americans decide to freeze their credit files). I suspect the pre-breach number is less than one percent. I base this guess loosely on some data I received from the head of security at Dropbox, who told KrebsOnSecurity last year that less than one percent of its user base of 500 million registered users had chosen to turn on 2-factor authentication for their accounts. This extra security step can block thieves from accessing your account even if they steal your password, but many consumers simply don’t take advantage of such offerings because either they don’t know about them or they find them inconvenient. Bear in mind that while most two-factor offerings are free, most freezes involve fees, so I’d expect the number of pre-breach freezers to be a fraction of one percent. However, if only one half of one percent of Americans chose to freeze their credit files before Equifax announced its breach — and if the total number of Americans requesting a freeze post-breach rose to, say, one percent — that would still be a huge jump (and potentially a painful financial hit to Equifax and the other bureaus).

So without further ado, here are some questions I’d ask on the topic of credit locks and freezes: -Approximately how many credit files on Americans does Equifax currently maintain? -Prior to the Equifax breach, approximately how many Americans had chosen to freeze their credit files at Equifax? -Approximately how many total Americans today have requested a freeze from Equifax? This should include the company’s best estimate on the number of people who have requested a freeze but — because of the many failings of Equifax’s public response cited by Barros — were unable to do so via phone or the Internet. -Approximately how much does Equifax charge each time the company sells a credit check (i.e., a bank or other potential creditor performs a “pull” on a consumer credit file)? -On average, how many times per year does Equifax sell access to consumer’s credit file to a potential creditor? -Mr. Barros said Equifax will extend its offer of free credit freezes until the end of January 2018. Why not make them free indefinitely, just as the company says it plans to do with its credit lock service? -In what way does a consumer placing a freeze on their credit file limit Equifax’s ability to do business? -In what way does a consumer placing a lock on their credit file limit Equifax’s ability to do business? -If a lock accomplishes the same as a freeze, why create more terminology that only confuses consumers? -By agreeing to use Equifax’s lock service, will consumers also be opting in to any additional marketing arrangements, either via Equifax or any of its partners? BREACH RESPONSEEquifax could hardly have bungled their breach response more if they tried. It is said that one should never attribute to malice what can more easily be explained by incompetence, but Equifax surely should have known that how they handled their public response would be paramount to their ability to quickly put this incident behind them and get back to business as usual.

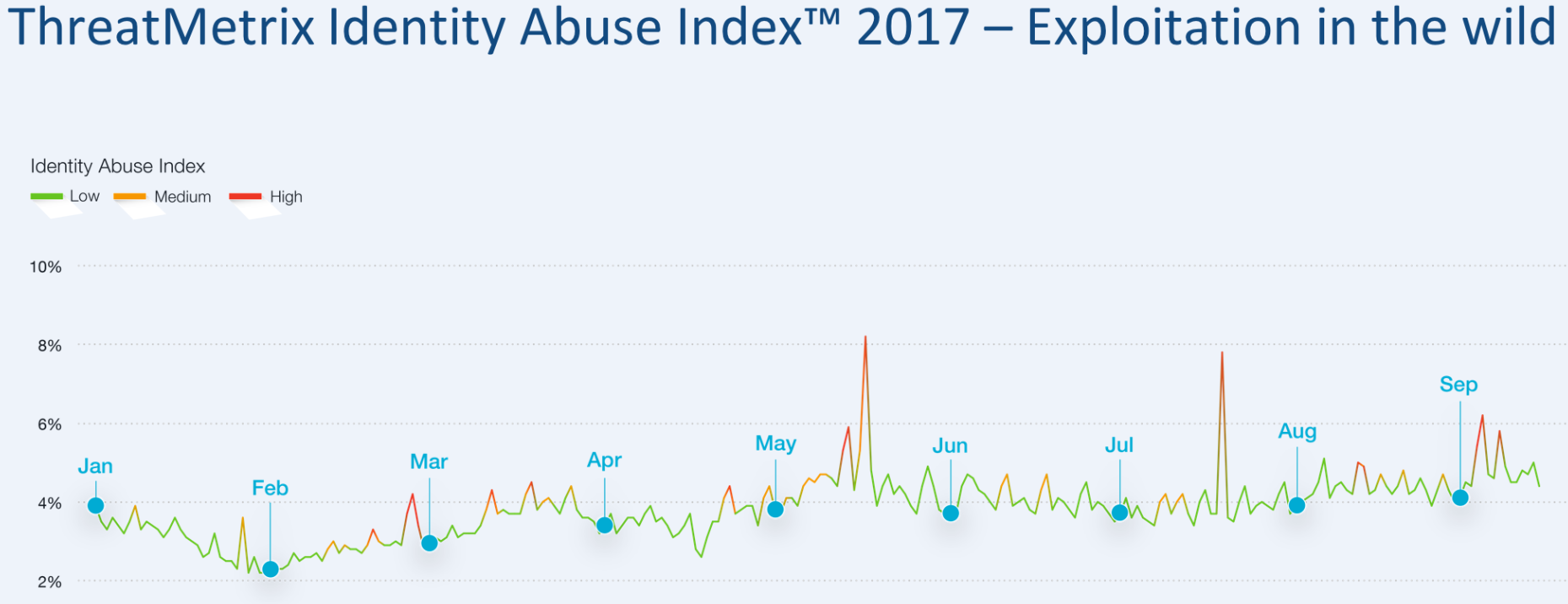

Equifax has come under heavy criticism for waiting too long to disclose this breach. It has said that the company became aware of the intrusion on July 29, and yet it did not publicly disclose the breach until Sept. 7.However, when Equifax did disclose, it seemed like everything about the response was rushed and ill-conceived. One theory that I simply cannot get out of my head is that perhaps Equifax rushed preparations for is breach disclosure and response because it was given a deadline by extortionists who were threatening to disclose the breach on their own if the company did not comply with some kind of demand. -I’d ask a question of mine that Equifax refused to answer shortly after the breach: Whether the company was the target of extortionists over this data breach *before* the breach was officially announced on Sept. 7. -Equifax said the attackers abused a vulnerability in Apache Struts to break in to the company’s Web applications. That Struts flaw was patched by the Apache Foundation on March 8, 2017, but Equifax waited until after July 30, 2017 — after it learned of the breach — to patch the vulnerability. Why did Equifax decide to wait four and a half months to apply this critical update? -How did Equifax become aware of this breach? Was it from an external source, such as law enforcement? -Assuming Equifax learned about this breach from law enforcement agencies, what did those agencies say regarding how they learned about the breach? FRAUD AND ABUSEMultiple news organizations have reported that companies which track crimes related to identity theft — such as account takeovers, new account fraud, and e-commerce fraud — saw huge upticks in all of these areas corresponding to two periods that are central to Equifax’s breach timeline; the first in mid-May, when Equifax said the intruders began abusing their access to the company, and the second late July/early August, when Equifax said it learned about the breach.

This chart shows spikes in various forms of identity abuse — including account takeovers and new account fraud — as tracked by ThreatMetrix, a San Jose, Calif. firm that helps businesses prevent fraud. -Has Equifax performed any analysis on consumer credit reports to determine if there has been any pattern of consumer harm as a result of this breach? -Assuming the answer to the previous question is yes, did the company see any spikes in applications for new lines of consumer credit corresponding to these two time periods in 2017? Many fraud experts report that a fast-growing area of identity theft involves so-called “synthetic ID theft,” in which fraudsters take data points from multiple established consumer identities and merge them together to form a new identity. This type of fraud often takes years to result in negative consequences for consumers, and very often the debt collection agencies will go after whoever legitimately owns the Social Security number used by that identity, regardless of who owns the other data points. -Is Equifax aware of a noticeable increase in synthetic identity theft in recent months or years? -What steps, if any, does Equifax take to ensure that multiple credit files are not using the same Social Security number? -Prior to its breach disclosure, Equifax spent more than a half million dollars in the first half of 2017 lobbying Congress to pass legislation that would limit the legal liability of credit bureaus in connection with data security lapses. Do you still believe such legislation is necessary? Why or why not? What questions did I leave out, Dear Readers? Or is there a way to make a question above more succinct? Sound off in the comments below, and I may just add yours to the list! In the meantime, here are the committees at which Former Equifax CEO Richard Smith will be testifying next week on Capitol Hill. Some of these committees will no doubt be live-streaming the hearings. Check back at the links below on the morning-of for more information on that. Also, C-SPAN almost certainly will be streaming some of these as well: -Tuesday, Oct. 3, 10:00 a.m., House Energy and Commerce Committee. Rayburn House Office Bldg. Room 2123. -Wednesday, Oct. 5, 10:00 a.m., Senate Committee on Banking, Housing, & Urban Affairs. Dirksen Senate Office Bldg., Room 538. -Wednesday, Oct. 5, 2:30 p.m., Senate Judiciary Subcommittee on Privacy, Technology and the Law. Dirksen Senate Office Bldg., Room 226. -Thursday, Oct. 6, 9:15 a.m., House Financial Services Committee. Rayburn House Office Bldg., Room 2128. from https://krebsonsecurity.com/2017/09/heres-what-to-ask-the-former-equifax-ceo/ Sonic Drive-In, a fast-food chain with nearly 3,600 locations across 45 U.S. states, has acknowledged a breach affecting an unknown number of store payment systems. The ongoing breach may have led to a fire sale on millions of stolen credit and debit card accounts that are now being peddled in shadowy underground cybercrime stores, KrebsOnSecurity has learned.

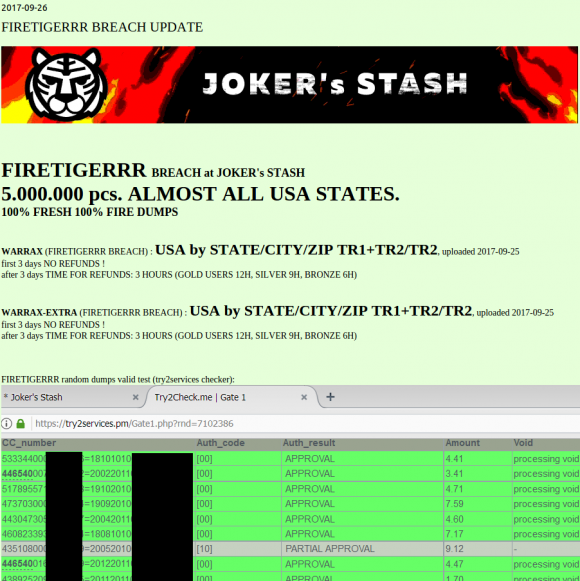

The first hints of a breach at Oklahoma City-based Sonic came last week when I began hearing from sources at multiple financial institutions who noticed a recent pattern of fraudulent transactions on cards that had all previously been used at Sonic. I directed several of these banking industry sources to have a look at a brand new batch of some five million credit and debit card accounts that were first put up for sale on Sept. 18 in a credit card theft bazaar previously featured here called Joker’s Stash:

This batch of some five million cards put up for sale today (Sept. 26, 2017) on the popular carding site Joker’s Stash has been tied to a breach at Sonic Drive-In. The first batch of these cards appear to have been uploaded for sale on Sept. 15. Sure enough, two sources who agreed to purchase a handful of cards from that batch of accounts on sale at Joker’s discovered they all had been recently used at Sonic locations. Armed with this information, I phoned Sonic, which responded within an hour that it was indeed investigating “a potential incident” at some Sonic locations. “Our credit card processor informed us last week of unusual activity regarding credit cards used at SONIC,” reads a statement the company issued to KrebsOnSecurity. “The security of our guests’ information is very important to SONIC. We are working to understand the nature and scope of this issue, as we know how important this is to our guests. We immediately engaged third-party forensic experts and law enforcement when we heard from our processor. While law enforcement limits the information we can share, we will communicate additional information as we are able.” Christi Woodworth, vice president of public relations at Sonic, said the investigation is still in its early stages, and the company does not yet know how many or which of its stores may be impacted. The accounts apparently stolen from Sonic are part of a batch of cards that Joker’s Stash is calling “Firetigerrr,” and they are indexed by city, state and ZIP code. This geographic specificity allows potential buyers to purchase only cards that were stolen from Sonic customers who live near them, thus avoiding a common anti-fraud defense at banks in which a financial institution might block out-of-state transactions from a known compromised card. Malicious hackers typically steal credit card data from organizations that accept cards by hacking into point-of-sale systems remotely and seeding those systems with malicious software that can copy account data stored on a card’s magnetic stripe. Thieves can then use that data to clone the cards and use the counterfeit cards to buy high-priced merchandise from electronics stores and big box retailers. Prices for the cards advertised in the Firetigerr batch are somewhat higher than for cards stolen in other breaches, likely because this batch is extremely fresh and unlikely to have been canceled by card-issuing banks yet.

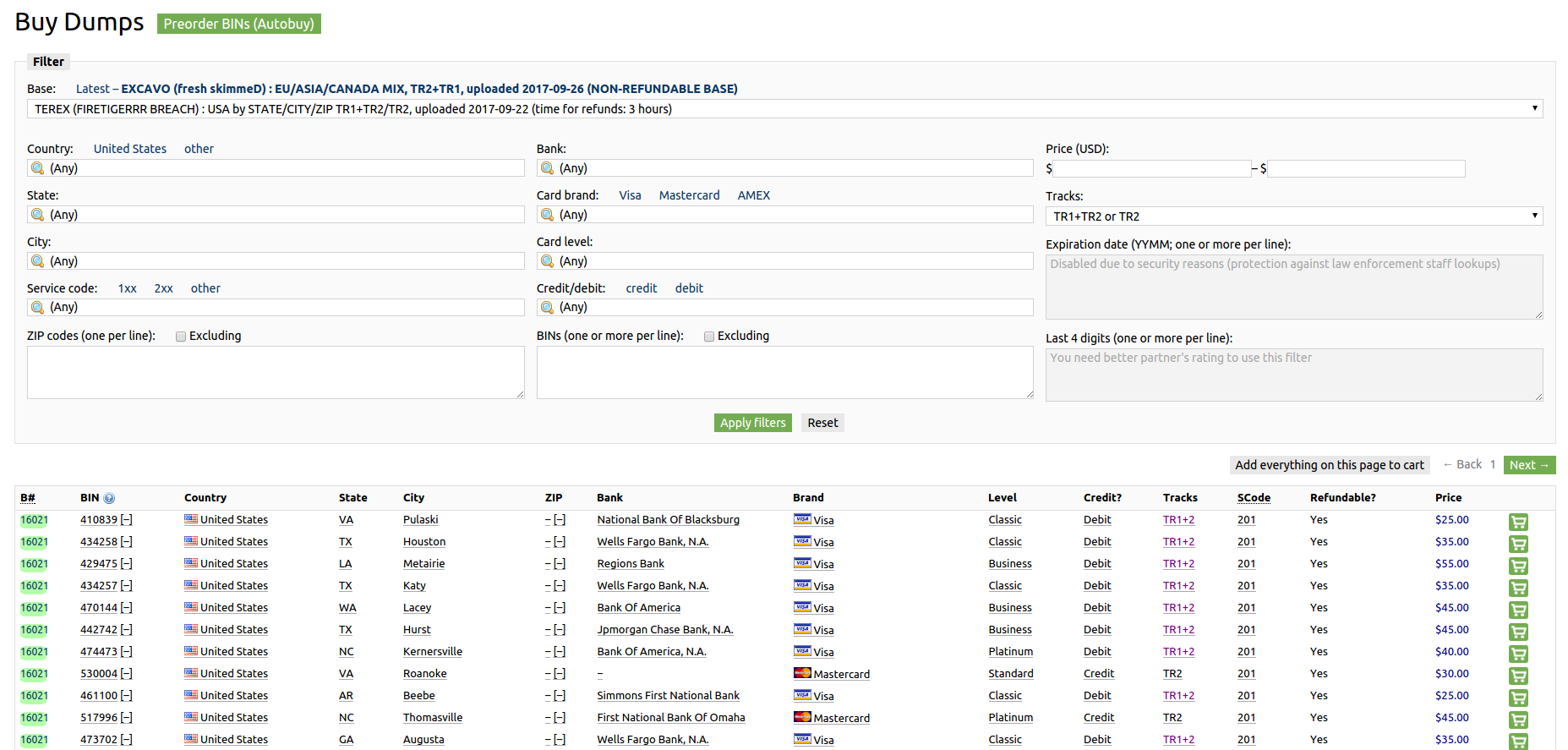

Dumps available for sale on Joker’s Stash from the “FireTigerrr” base, which has been linked to a breach at Sonic Drive-In. Click image to enlarge. Most of the cards range in price from $25 to $50, and the price is influenced by a number of factors, including: the type of card issued (Amex, Visa, MasterCard, etc); the card’s level (classic, standard, signature, platinum, etc.); whether the card is debit or credit; and the issuing bank. I should note that it remains unclear whether Sonic is the only company whose customers’ cards are being sold in this particular batch of five million cards at Joker’s Stash. There are some (as yet unconfirmed) indications that perhaps Sonic customer cards are being mixed in with those stolen from other eatery brands that may be compromised by the same attackers. The last known major card breach involving a large nationwide fast-food chain impacted more than a thousand Wendy’s locations and persisted for almost nine months after it was first disclosed here. The Wendy’s breach was extremely costly for card-issuing banks and credit unions, which were forced to continuously re-issue customer cards that kept getting re-compromised every time their customers went back to eat at another Wendy’s. Part of the reason Wendy’s corporate offices had trouble getting a handle on the situation was that most of the breached locations were not corporate-owned but instead independently-owned franchises whose payment card systems were managed by third-party point-of-sale vendors. According to Sonic’s Wikipedia page, roughly 90 percent of Sonic locations across America are franchised. Dan Berger, president and CEO of the National Association of Federally Insured Credit Unions, said he’s not looking forward to the prospect of another Wendy’s-like fiasco. “It’s going to be the financial institution that makes them whole, that pays off the charges or replaces money in the customer’s checking account, or reissues the cards, and all those costs fall back on the financial institutions,” Berger said. “These big card breaches are going to continue until there’s a national standard that holds retailers and merchants accountable.” Financial institutions also bear some of the blame for the current state of affairs. The United States is embarrassingly the last of the G20 nations to make the shift to more secure chip-based cards, which are far more expensive and difficult for criminals to counterfeit. But many financial institutions still haven’t gotten around to replacing traditional magnetic stripe cards with chip-based cards. According to Visa, 58 percent of the more than 421 million Visa cards issued by U.S. financial institutions were chip-based as of March 2017. Likewise, retailers that accept chip cards may present a less attractive target to hackers than those that don’t. In March 2017, Visa said the number of chip-enabled merchant locations in the country reached two million, representing 44 percent of stores that accept Visa. from https://krebsonsecurity.com/2017/09/breach-at-sonic-drive-in-may-have-impacted-millions-of-credit-debit-cards/ Deloitte, one of the world’s “big four” accounting firms, has acknowledged a breach of its internal email systems, British news outlet The Guardian revealed today. Deloitte has sought to downplay the incident, saying it impacted “very few” clients. But according to a source close to the investigation, the breach dates back to at least the fall of 2016, and involves the compromise of all administrator accounts at the company as well as Deloitte’s entire internal email system.

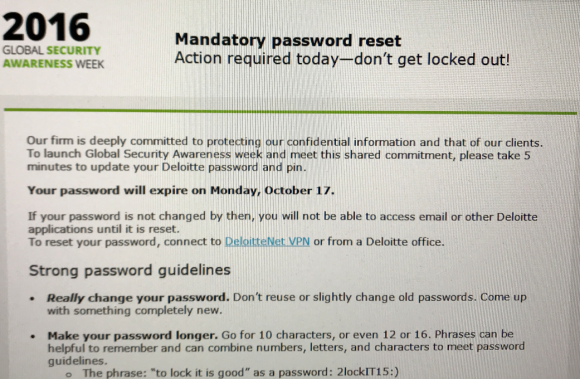

In a story published Monday morning, The Guardian said a breach at Deloitte involved usernames, passwords and personal data on the accountancy’s top blue-chip clients. “The Guardian understands Deloitte clients across all of these sectors had material in the company email system that was breached,” The Guardian’s Nick Hopkins wrote. “The companies include household names as well as US government departments. So far, six of Deloitte’s clients have been told their information was ‘impacted’ by the hack.” In a statement sent to KrebsOnSecurity, Deloitte acknowledged a “cyber incident” involving unauthorized access to its email platform. “The review of that platform is complete,” the statement reads. “Importantly, the review enabled us to understand precisely what information was at risk and what the hacker actually did and to determine that only very few clients were impacted [and] no disruption has occurred to client businesses, to Deloitte’s ability to continue to serve clients, or to consumers.” However, information shared by a person with direct knowledge of the incident said the company in fact does not yet know precisely when the intrusion occurred, or for how long the hackers were inside of its systems. This source, speaking on condition of anonymity, said the team investigating the breach focused their attention on a company office in Nashville known as the “Hermitage,” where the breach is thought to have begun. The source confirmed The Guardian reporting that current estimates put the intrusion sometime in the fall of 2016, and added that investigators still are not certain that they have completely evicted the intruders from the network. Indeed, it appears that Deloitte has known something was not right for some time. According to this source, the company sent out a “mandatory password reset” email on Oct. 13, 2016 to all Deloitte employees in the United States. The notice stated that employee passwords and personal identification numbers (PINs) needed to be changed by Oct. 17, 2016, and that employees who failed to do so would be unable to access email or other Deloitte applications. The message also included advice on how to pick complex passwords:

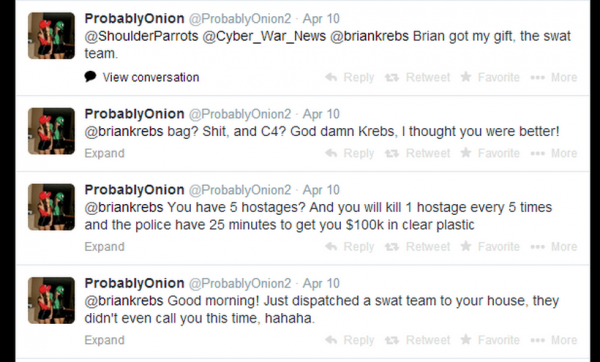

A screen shot of the mandatory password reset email Deloitte sent to all U.S. employees in Oct. 2016, around the time sources say the breach was first discovered. The source told KrebsOnSecurity they were coming forward with information about the breach because, “I think it’s unfortunate how we have handled this and swept it under the rug. It wasn’t a small amount of emails like reported. They accessed the entire email database and all admin accounts. But we never notified our advisory clients or our cyber intel clients.” “Cyber intel” refers to Deloitte’s Cyber Intelligence Centre, which provides 24/7 “business-focused operational security” to a number of big companies, including CSAA Insurance, FedEx, Invesco, and St. Joseph’s Healthcare System, among others. This same source said forensic investigators identified several gigabytes of data being exfiltrated to a server in the United Kingdom. The source further said the hackers had free reign in the network for “a long time” and that the company still does not know exactly how much total data was taken. In its statement about the incident, Deloitte said it responded by “implementing its comprehensive security protocol and initiating an intensive and thorough review which included mobilizing a team of cyber-security and confidentiality experts inside and outside of Deloitte.” Additionally, the company said it contacted governmental authorities immediately after it became aware of the incident, and that it contacted each of the “very few clients impacted.” “Deloitte remains deeply committed to ensuring that its cyber-security defenses are best in class, to investing heavily in protecting confidential information and to continually reviewing and enhancing cyber security,” the statement concludes. Deloitte has not yet responded to follow-up requests for comment. The Guardian reported that Deloitte notified six affected clients, but Deloitte has not said publicly yet when it notified those customers. Deloitte has a significant cybersecurity consulting practice globally, wherein it advises many of its clients on how best to secure their systems and sensitive data from hackers. In 2012, Deloitte was ranked #1 globally in security consulting based on revenue. Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company based in the United Kingdom. According to the company’s Web site, Deloitte has more than 263,000 employees at member firms delivering services in audit and insurance, tax, consulting, financial advisory, risk advisory, and related services in more than 150 countries and territories. Revenues for the fiscal year 2017 were $38.8 billion. The breach at the big-four accountancy comes on the heels of a massive breach at big-three consumer credit bureau Equifax. That incident involved several months of unauthorized access in which intruders stole Social Security numbers, birth dates, and addresses on 143 million Americans. This is a developing story. Any updates will be posted as available, and noted with update timestamps. from https://krebsonsecurity.com/2017/09/source-deloitte-breach-affected-all-company-email-admin-accounts/ A 19-year-old Canadian man was found guilty of making almost three dozen fraudulent calls to emergency services across North America in 2013 and 2014. The false alarms, two of which targeted this author — involved phoning in phony bomb threats and multiple attempts at “swatting” — a dangerous hoax in which the perpetrator spoofs a call about a hostage situation or other violent crime in progress in the hopes of tricking police into responding at a particular address with deadly force. Curtis Gervais of Ottawa was 16 when he began his swatting spree, which prompted police departments across the United States and Canada to respond to fake bomb threats and active shooter reports at a number of schools and residences. Gervais, who taunted swatting targets using the Twitter accounts “ProbablyOnion” and “ProbablyOnion2,” got such a high off of his escapades that he hung out a for-hire shingle on Twitter, offering to swat anyone with the following tweet:

Several Twitter users apparently took him up on that offer. On March 9, 2014, @ProbablyOnion started sending me rude and annoying messages on Twitter. A month later (and several weeks after blocking him on Twitter), I received a phone call from the local police department. It was early in the morning on Apr. 10, and the cops wanted to know if everything was okay at our address. Since this was not the first time someone had called in a fake hostage situation at my home, the call I received came from the police department’s non-emergency number, and they were unsurprised when I told them that the Krebs manor and all of its inhabitants were just fine. Minutes after my local police department received that fake notification, @ProbablyOnion was bragging on Twitter about swatting me, including me on his public messages: “You have 5 hostages? And you will kill 1 hostage every 6 times and the police have 25 minutes to get you $100k in clear plastic.” Another message read: “Good morning! Just dispatched a swat team to your house, they didn’t even call you this time, hahaha.”

I told this user privately that targeting an investigative reporter maybe wasn’t the brightest idea, and that he was likely to wind up in jail soon. On May 7, @ProbablyOnion tried to get the swat team to visit my home again, and once again without success. “How’s your door?” he tweeted. I replied: “Door’s fine, Curtis. But I’m guessing yours won’t be soon. Nice opsec!” I was referring to a document that had just been leaked on Pastebin, which identified @ProbablyOnion as a 19-year-old Curtis Gervais from Ontario. @ProbablyOnion laughed it off but didn’t deny the accuracy of the information, except to tweet that the document got his age wrong. A day later, @ProbablyOnion would post his final tweet before being arrested: “Still awaiting for the horsies to bash down my door,” a taunting reference to the Royal Canadian Mounted Police (RCMP). A Sept. 14, 2017 article in the Ottawa Citizen doesn’t name Gervais because it is against the law in Canada to name individuals charged with or convicted of crimes committed while they are a minor. But the story quite clearly refers to Gervais, who reportedly is now married and expecting a child. The Citizen says the teenager was arrested by Ottawa police after the U.S. FBI traced his Internet address to his parents’ home. The story notes that “the hacker” and his family have maintained his innocence throughout the trial, and that they plan to appeal the verdict. Gervais’ attorneys reportedly claimed the youth was framed by the hacker collective Anonymous, but the judge in the case was unconvinced. Apparently, U.S. Ontario Court Justice Mitch Hoffman handed down a lenient sentence in part because of more than 900 hours of volunteer service the accused had performed in recent years. From the story:

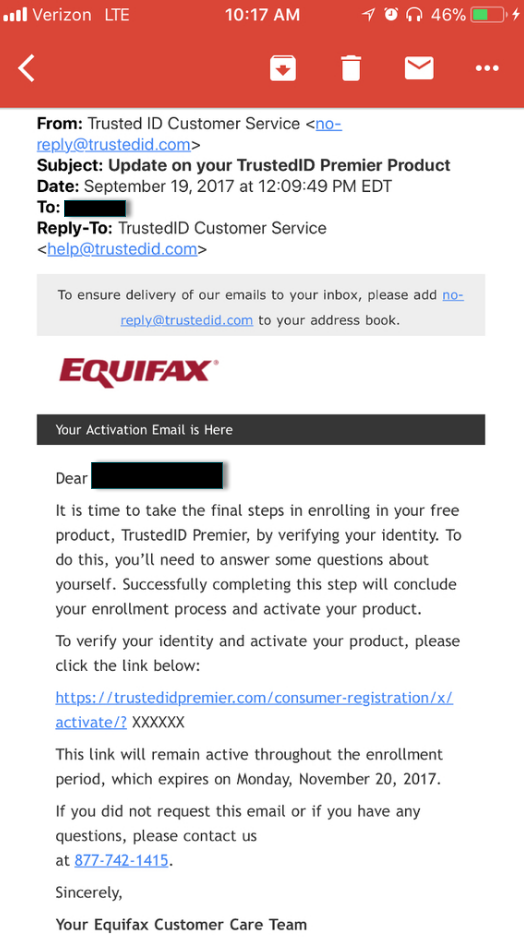

According to the article, the teen will serve six months of his nine-month sentence at a youth group home and three months at home “under strict restrictions, including the forfeiture of a home computer used to carry out the cyber pranks.” He also is barred from using Twitter or Skype during his 18-month probation period. Most people involved in swatting and making bomb threats are young males under the age of 18 — the age when kids seem to have little appreciation for or care about the seriousness of their actions. According to the FBI, each swatting incident costs emergency responders approximately $10,000. Each hoax also unnecessarily endangers the lives of the responders and the public. In February 2017, another 19-year-old — a man from Long Beach, Calif. named Eric “Cosmo the God” Taylor — was sentenced to three year’s probation for his role in swatting my home in Northern Virginia in 2013. Taylor was among several men involved in making a false report to my local police department at the time about a supposed hostage situation at our house. In response, a heavily-armed police force surrounded my home and put me in handcuffs at gunpoint before the police realized it was all a dangerous hoax. from https://krebsonsecurity.com/2017/09/canadian-man-gets-9-months-detention-for-serial-swattings-bomb-threats/ More than a week after it said most people would be eligible to enroll in a free year of its TrustedID identity theft monitoring service, big three consumer credit bureau Equifax has begun sending out email notifications to people who were able to take the company up on its offer. But in yet another security stumble, the company appears to be training recipients to fall for phishing scams. Some people who signed up for the service after Equifax announced Sept. 7 that it had lost control over Social Security numbers, dates of birth and other sensitive data on 143 million Americans are still waiting for the promised notice from Equifax. But as I recently noted on Twitter, other folks have received emails from Equifax over the past few days, and the messages do not exactly come across as having emanated from a company that cares much about trying to regain the public’s trust. Here’s a redacted example of an email Equifax sent out to one recipient recently:

As we can see, the email purports to have been sent from trustedid.com, a domain that Equifax has owned for almost four years. However, Equifax apparently decided it was time for a new — and perhaps snazzier — name: trustedidpremier.com. The above-pictured message says it was sent from one domain, and then asks the recipient to respond by clicking on a link to a completely different (but confusingly similar) domain. My guess is the reason Equifax registered trustedidpremier.com was to help people concerned about the breach to see whether they were one of the 143 million people affected (for more on how that worked out for them, see Equifax Breach Response Turns Dumpster Fire). I’d further surmise that Equifax was expecting (and received) so much interest in the service as a result of the breach that all the traffic from the wannabe customers might swamp the trustedid.com site and ruin things for the people who were already signed up for the service before Equifax announced the breach on Sept. 7. The problem with this dual-domain approach is that the domain trustedidpremier.com is only a few weeks old, so it had very little time to establish itself as a legitimate domain. As a result, in the first few hours after Equifax disclosed the breach the domain was actually flagged as a phishing site by multiple browsers because it was brand new and looked about as professionally designed as a phishing site. What’s more, there is nothing tying the domain registration records for trustedidpremier.com to Equifax: The domain is registered to a WHOIS privacy service, which masks information about who really owns the domain (again, not exactly something you might expect from an identity monitoring site). Anyone looking for assurances that the site perhaps was hosted on Internet address space controlled by and assigned to Equifax would also be disappointed: The site is hosted at Amazon. While there’s nothing wrong with that exactly, one might reasonably ask: Why didn’t Equifax just send the email from Equifax.com and host the ID theft monitoring service there as well? Wouldn’t that have considerably lessened any suspicion that this missive might be a phishing attempt? Perhaps, but you see while TrustedID is technically owned by Equifax Inc., its services are separate from Equifax and its terms of service are different from those provided by Equifax (almost certainly to separate Equifax from any consumer liability associated with its monitoring service). THE BACKSTORYWhat’s super-interesting about trustedid.com is that it didn’t always belong to Equifax. According to the site’s Wikipedia page, TrustedID Inc. was purchased by Equifax in 2013, but it was founded in 2004 as an identity protection company which offered a service that let consumers automatically “freeze” their credit file at the major bureaus. A freeze prevents Equifax and the other major credit bureaus from selling an individual’s credit data without first getting consumer consent. By 2006, some 17 states offered consumers the ability to freeze their credit files, and the credit bureaus were starting to see the freeze as an existential threat to their businesses (in which they make slightly more than a dollar each time a potential creditor — or ID thief — asks to peek at your credit file). Other identity monitoring firms — such as LifeLock — were by then offering services that automated the placement of identity fraud controls — such as the “fraud alert,” a free service that consumers can request to block creditors from viewing their credit files. [Author’s note: Fraud alerts only last for 90 days, although you can renew them as often as you like. More importantly, while lenders and service providers are supposed to seek and obtain your approval before granting credit in your name if you have a fraud alert on your file, they are not legally required to do this — and very often don’t.] Anyway, the era of identity monitoring services automating things like fraud alerts and freezes on behalf of consumers effectively died after a landmark lawsuit filed by big-three bureau Experian (which has its own storied history of data breaches). In 2008, Experian sued LifeLock, arguing its practice of automating fraud alerts violated the Fair Credit Reporting Act. In 2009, a court found in favor of Experian, and that decision effectively killed such services — mainly because none of the banks wanted to distribute them and sell them as a service anymore. WHAT SHOULD YOU DOThese days, consumers in all states have a right to freeze their credit files, and I would strongly encourage all readers to do this. Yes, it can be a pain, and the bureaus certainly seem to be doing everything they can at the moment to make this process extremely difficult and frustrating for consumers. As detailed in the analysis section of last week’s story — Equifax Breach: Setting the Record Straight — many of the freeze sites are timing out, crashing or telling consumers just to mail in copies of identity documents and printed-out forms. Other bureaus, like TransUnion and Experian, are trying mightily to steer consumers away from a freeze and toward their confusingly named “credit lock” services — which claim to be the same thing as freezes only better. The truth is these lock services do not prevent the bureaus from selling your credit reports to anyone who comes asking for them (including ID thieves); and consumers who opt for them over freezes must agree to receive a flood of marketing offers from a myriad of credit bureau industry partners. While it won’t stop all forms of identity theft (such as tax refund fraud or education loan fraud), a freeze is the option that puts you the consumer in the strongest position to control who gets to monkey with your credit file. In contrast, while credit monitoring services might alert you when someone steals your identity, they’re not designed to prevent crooks from doing so. That’s not to say credit monitoring services aren’t useful: They can be helpful in recovering from identity theft, which often involves a tedious, lengthy and expensive process for straightening out the phony activity with the bureaus. The thing is, it’s almost impossible to sign up for credit monitoring services while a freeze is active on your credit file, so if you’re interested in signing up for them it’s best to do so before freezing your credit. But there’s no need to pay for these services: Hundreds of companies — many of which you have probably transacted with at some point in the last year — have disclosed data breaches and are offering free monitoring. California maintains one of the most comprehensive lists of companies that disclosed a breach, and most of those are offering free monitoring. There’s a small catch with the freezes: Depending on the state in which you live, the bureaus may each be able to charge you for freezing your file (the fee ranges from $5 to $20); they may also be able to charge you for lifting or temporarily thawing your file in the event you need access to credit. Consumers Union has a decent rundown of the freeze fees by state. In short, sign up for whatever free monitoring is available if that’s of interest, and then freeze your file at the four major bureaus. You can do this online, by phone, or through the mail. Given how unreliable the credit bureau Web sites have been for placing freezes these past few weeks, it may be easiest to do this over the phone. Here are the freeze Web sites and freeze phone numbers for each bureau (note the phone procedures can and likely will change as the bureaus get wise to more consumers learning how to quickly step through their automated voice response systems): Equifax: 866-349-5191; choose option 3 for a “Security Freeze” Experian: 888-397-3742; Innovis: 800-540-2505; Transunion: 888-909-8872, choose option 3 If you still have questions about freezes, fraud alerts, credit monitoring or anything else related to any of the above, check out the lengthy primer/Q&A I published here on Sept. 11, The Equifax Breach: What You Should Know. from https://krebsonsecurity.com/2017/09/equifax-or-equiphish/ |

ABOUT MEHi my name is Anthony I am 32 years old from Houston. I am working in local store selling electronic devices. I have been interested in eclectronics since childhood and I like to reacd about it. Archives

April 2019

Categories |

RSS Feed

RSS Feed